Retiring Alone? Don't Let Divorce Wipe Out Your Pension.

The rules change after 50. We help you value, divide, and protect your OMERS, OTPP, and private investments correctly.

Actuarial Valuation vs. Statement Value explained

Prevent the "Double-Dip" on pension income

Protect 30+ years of retirement planning

Get the Valuation Guide + Spousal Support Matrix

Understand exactly what your pension is worth—and how to protect it.

Senior Counsel Warning:

"I often see spouses settle for 'Statement Value' on a pension, losing hundreds of thousands of dollars. This guide explains why you need an Actuarial Valuation, not just a bank statement."

— Deepa Tailor, Senior Family Lawyer

Why "50/50" Isn't Always Fair in Grey Divorce

After decades of building retirement security, these three hidden risks can cost you hundreds of thousands—if you don't know what to look for.

1. The Valuation Gap

The number on your monthly pension statement is NOT the same as its true value in a divorce. The "Commuted Value" (what it would cost to buy that income stream) is often 2-3x higher than the statement balance.

Real-World Impact: Example: Your OMERS statement shows $400,000. The actuarial commuted value? $1.2 million. That is an $800,000 mistake if you settle without proper valuation.

2. The Double-Dip

Your pension can be counted twice in divorce: once as an asset to be divided, and again as income for calculating spousal support. Without proper legal structuring, you could pay support based on income you have already split.

Real-World Impact: The Fix: Our guide shows you how to use the "Boston Formula" or "if-and-when" method to prevent this costly double-counting.

3. The Insurance Trap

Many workplace pensions include health benefits and life insurance that terminate upon divorce. If you are over 55 with pre-existing conditions, replacing this coverage privately can cost $500-$1,500/month—or be impossible to obtain.

Real-World Impact: The Strategy: Negotiate to keep spousal coverage as part of the settlement, or factor replacement costs into your support calculations.

Don't navigate these risks alone. Get the complete breakdown in our free guide.

Download the Pension Protection KitWhat's Inside the Kit

Three practical tools designed specifically for divorcing spouses over 50 with significant retirement assets.

Download to Unlock

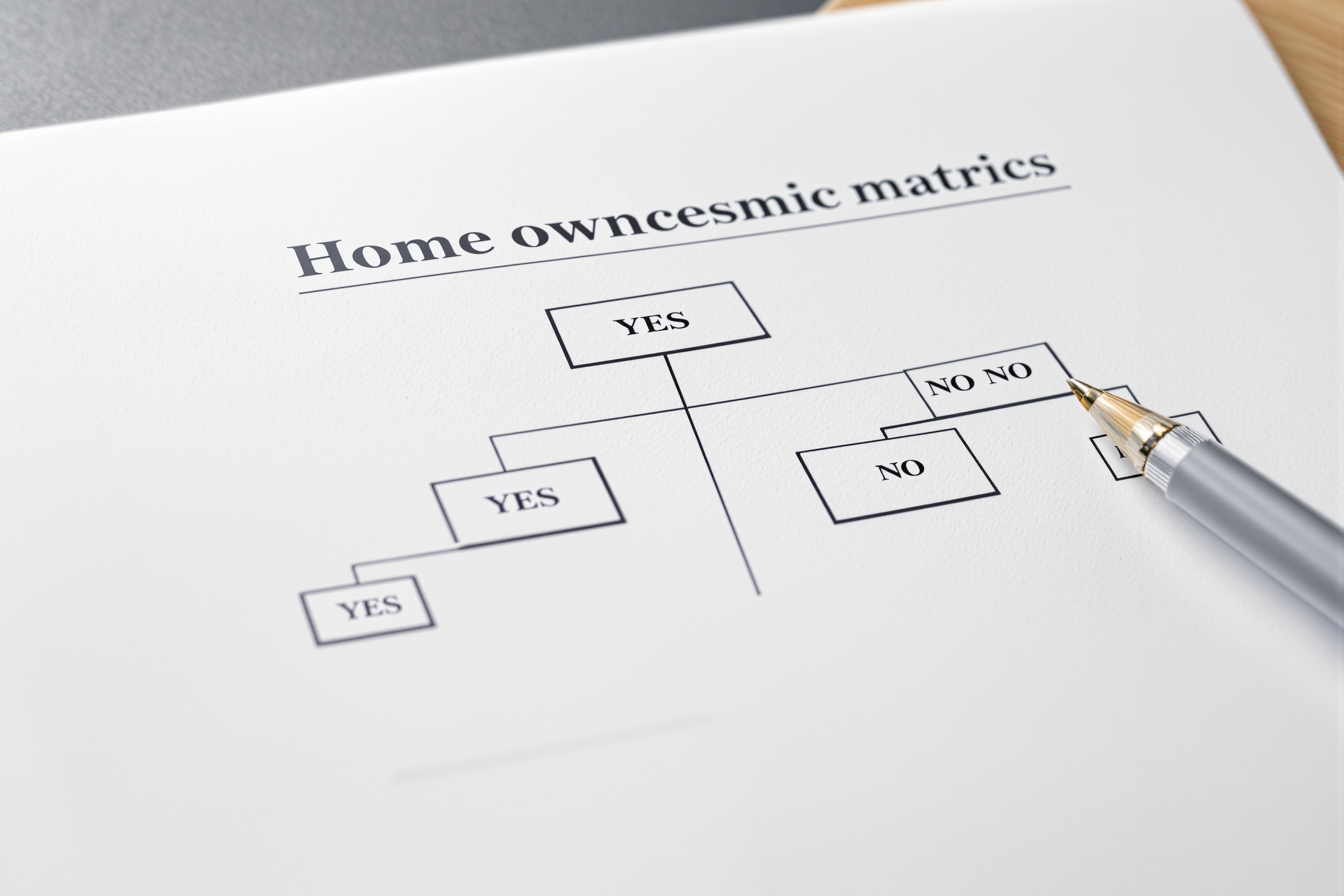

The "Stay or Sell" Matrix

A decision tree for the Matrimonial Home. Should you buy out your spouse, sell and split, or defer the sale? This flowchart walks you through tax implications, capital gains, and cash flow scenarios.

Download to Unlock

The Pension Checklist

Exactly what to ask your Plan Administrator. This one-page checklist ensures you request the correct valuation documents (Commuted Value, Survivor Benefits, Early Retirement Penalties) the first time.

Download to Unlock

The "Grey" Spousal Support Calculator

How retirement dates impact support duration. Use this calculator to model different scenarios: retiring at 60 vs. 65, lump-sum buyouts, and how pension income affects monthly support obligations.

Plus: The "30-Year Rule" Explainer

Understand how the length of your marriage affects pension division, spousal support duration, and your negotiating position. This bonus section includes case law examples and settlement strategies.

Your retirement took 30 years to build. Protect it.

Don't let a rushed settlement cost you hundreds of thousands. Get the tools and knowledge you need to negotiate from a position of strength.

Get the Free Guide